The number of golf facilities operating in the US has remained stable for the past five years – at around 14,000 – representing 16,000 courses – according to the latest figures compiled by the National Golf Foundation.

This extended period of equilibrium follows a prolonged market correction that began in 2006, when closures first outpaced openings, culminating in a cumulative 13% reduction in courses after the recession of 2007-2009.

In recent years, closures in the US have fallen to their lowest levels since 2004, while modest new development, course resurrections, and significant renovation projects have contributed to improved financial health across the sector.

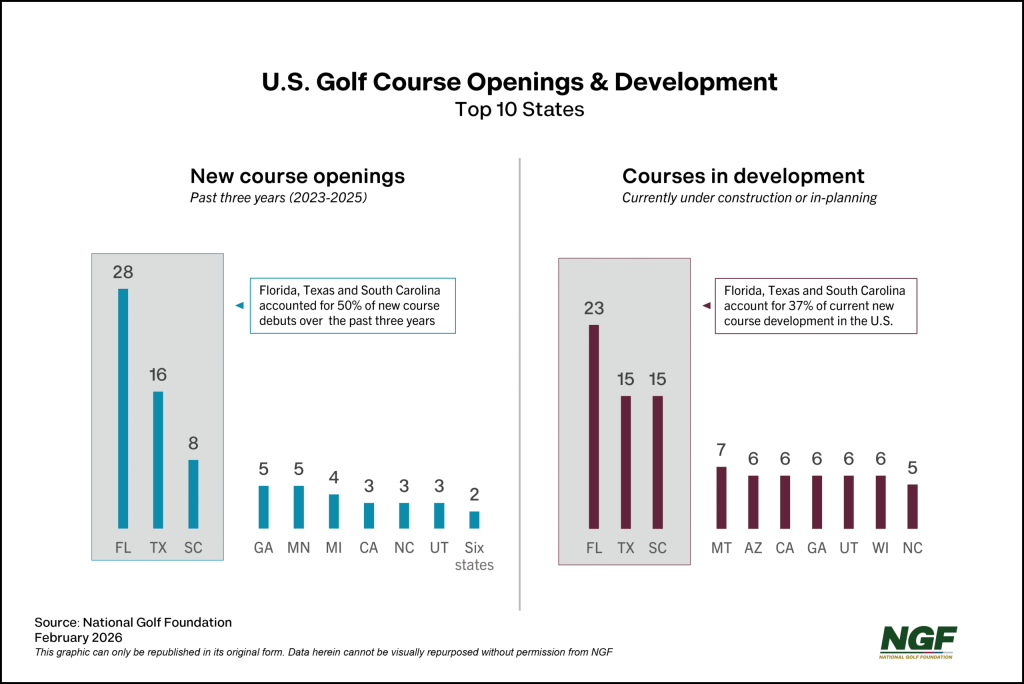

At the start of 2026, more than 140 new courses were in planning or under construction, with the majority tied to private destination clubs, high-end real estate communities, and resorts.

Florida, Texas, and South Carolina accounted for half of the new openings over the past three years and represent more than one-third of projects in the pipeline. Just over half of those projects are private, above the current US supply mix of 28% private and 78% public.